SchusterWatch #846 (6/15/2026)

Take Off: U.S. Equity Capital Markets buoyed by good SpaceX debut.

First broad index to track SpaceX: IPOX® 100 U.S. soars +4.18% last week.

Big Movers: NUVL, ALHC, ALMS, CRDO, SNDK, 9903 HK.

IPOs: SpaceX debut paves the way for series of large U.S. IPOs, OpenAI.

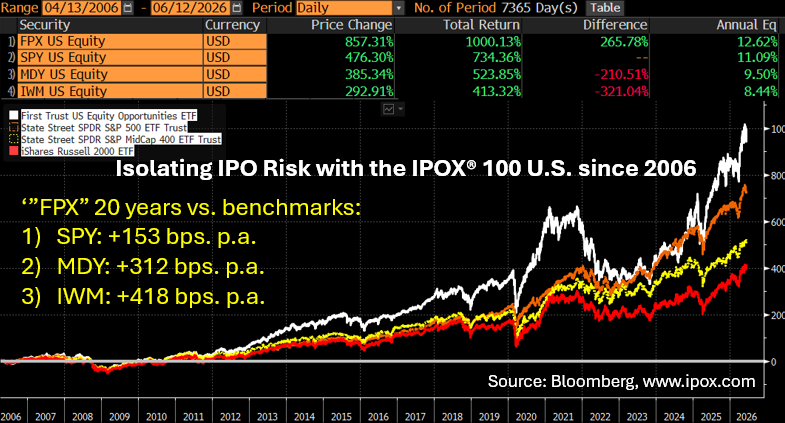

WEEKLY OVERVIEW: Equity markets rose last week, as earnings optimism and the big semiconductor trade trumped fears over war, inflation, and weakness in the electrification sector. The IPOX® Indexes were the main beneficiaries of the risk-on sentiment (VIX: -17.81%) and jumped. The IPOX® 100 U.S. (ETF: FPX) became the first broad-based index to add SpaceX (SPCX), with CME-listed E-mini IPOX® 100 U.S. Futures (IPOU6) being the first CME equity index product offering index-based access to the firm.

UNITED STATES: The IPOX® 100 U.S. Index (IPXO), tracked by the First Trust U.S. Equity Opportunities ETF (Ticker: FPX), surged +4.18% to +17.44% YTD, extending its YTD lead vs. the S&P 500 (SPX) — a benchmark for U.S. stocks — by +353 bps to +888 bps YTD. 65% of holdings rose, with the average (median) equally weighted firm adding +3.17% (+1.55%), lagging the applied market-cap-weighted index. Idiosyncratic returns delivered by our exposure to the takeover of portfolio firm biopharma Nuvalent (NUVL US: +35.51%) by British Large Pharma GSK (GSK US: +2.95%) provided the backdrop for the strong showing, which was further cemented by big gains in health care and technology exposure, including Alignment Healthcare (ALHC US: +28.50%), Sandisk (SNDK US: +26.98%), Alumis (ALMS US: +26.71%), and Credo Technology (CRDO US: +21.23%). A series of aging-out IPO stars lagged anew, including food delivery services Doordash (DASH US: -3.97%), intelligence software maker Palantir (PLTR US: -5.56%), and marketing AI solutions provider AppLovin (APP US: -11.96%).

INTERNATIONAL: The IPOX® International (IPXI), tracked by the First Trust International Equity Opportunities ETF (Ticker: FPXI), added +1.71% to +29.73% YTD last week, remaining +2135 bps ahead of the International Market YTD. Tech exposure traded on both sides of the return spectrum, with Chinese semiconductor maker Shanghai Illuvatar CoreX (9903 HK: +28.78%) leading, while AI play Knowledge Atlas (2513 HK: -15.42%) fell sharply. As in the U.S., the electrification trade continued to weaken here as well, with Germany’s Siemens Energy (ENR GY: -2.81%) in focus.

OUR NOVEL APPROACH TO SPACEX: Our investment philosophy is to pool New Listings into a separately tradable equity sector because the “going public” effects are real and truly unique to IPOs. This approach has helped us isolate the unique IPO risk while capturing the opportunities of the New Listings market:

THE IPOX® SPAC INDEX: Last week, the IPOX® SPAC Index gained +0.91% to +16.59% YTD. Biotech Tango Therapeutics (TNGX US: +53.02%) rose after reporting positive pancreatic cancer trial data. Battery developer Amprius Technologies (AMPX US: -17.17%) fell the most, without any material company-specific catalyst. Five SPACs announced merger targets, including Inflection Point Acquisition VI (IPFX US) with former NASA spacecraft developer Quantum Space, aiming to capitalize on growing investor interest in the space sector. Four SPACs completed business combinations, including Voyager Acquisition’s merger with Zurich-based cancer biotech Veraxa Biotech (VRXA US). 4 new SPACs launched in the U.S.

ECM REVIEW: 26 companies went public last week, raising a record-breaking $78.4 billion. New listings gained an average of +51.00% from offer price to Friday’s close (median: +11.94%). The week was dominated by SpaceX (SPCX US: +19.22%), which raised $75 billion. Other IPOs included Canadian drugmaker Apotex Health (APTX CN: +20.79%, $943 million), biotech Parabilis Medicines (PBLS US: +36.30%, $771 million), gas generator firm ERock (EROC US: -21.16%, $600 million), natural gas royalty firm WhiteHawk Minerals (WHK US: +4.96%, $200 million), Nordic installation services firm InstallatørGruppen (IG DC: -10.67%, $163 million), digital bank Forbright (FRBT US: 0.00%, $142 million), and Swedish industrial investor Tangen Industrikapital (TANGENB SS: +11.94%, $112 million). Amid the shortened U.S. trading week, the calendar includes Chinese food producer Liuliumei (6658 HK, $64 million), Japanese taxi app GO (581A JP, $548 million), furniture retailer Bohus (BOHUS NO, $98 million), Chinese sensor chip firm SENASIC (6675 HK, $125 million), biotech Kardigan (KARD US, $350 million), and community bank First Carolina Financial Services (FCBM US, $83 million).

IPOX IN THE NEWS: IPOX® was featured heavily in the financial media last week. Reuters cited IPOX® Associate Lukas Muehlbauer on U.S. biotechs Kardigan and Parabilis Medicines, as well as gas generator firm ERock, highlighting recovering issuance and continued investor selectivity on valuation. On the large-IPO theme and SpaceX, Germany’s largest weekly newspaper DIE ZEIT interviewed Muehlbauer on mega-IPO absorption risks, while Japan’s largest financial paper Nikkei spoke with IPOX® CEO Schuster. Reuters also quoted Schuster on OpenAI’s confidential IPO filing and the broader move of large AI companies toward public markets.