The IPOX® Week #640

Headlines

In big move, IPOX® 100 U.S. (ETF: FPX) soars +9.21% during July.

Surge extends to most markets abroad, China notable laggard.

IPOX® SPAC (SPAC) surges +12.20% last week. No SPACs launched.

4 Chinese firms crosslist in Switzerland. Little IPO deal flow seen this week.

Weekly Performance Review

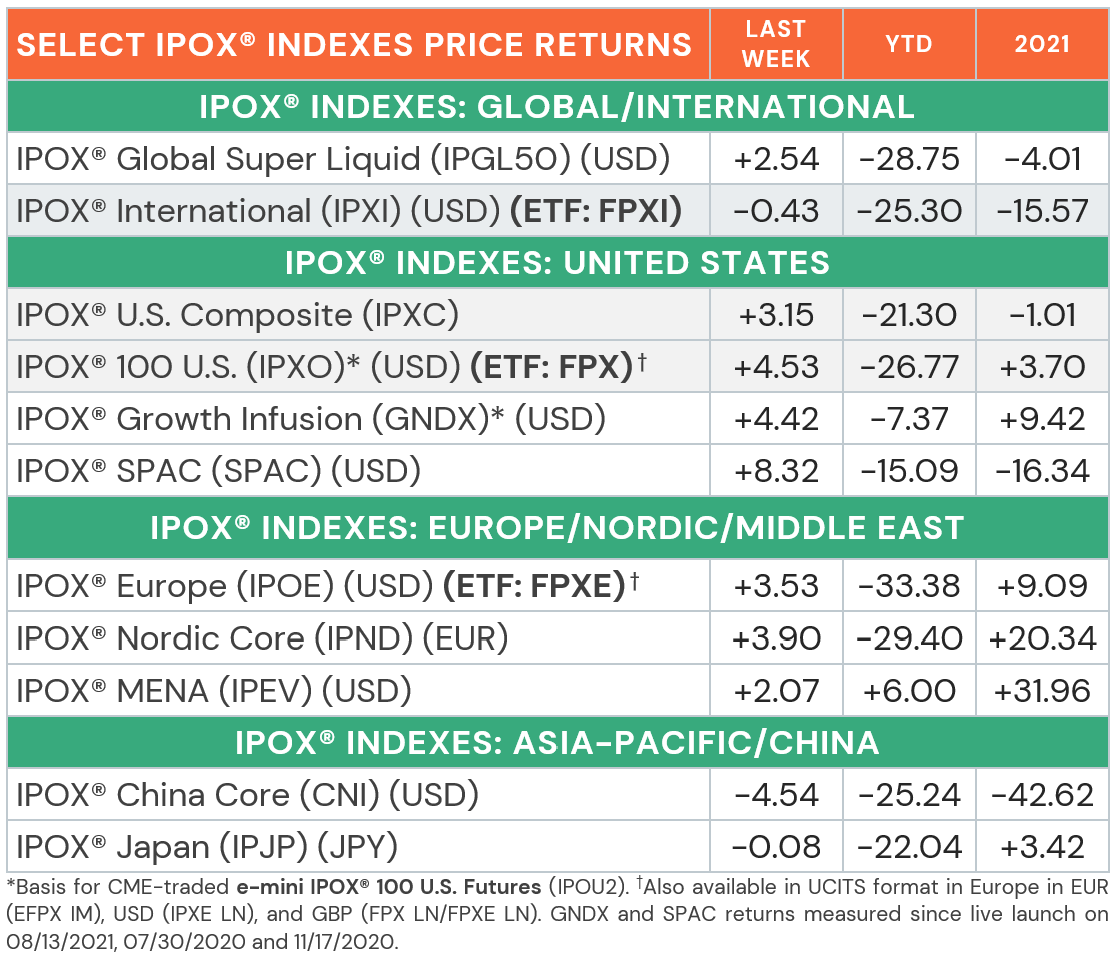

Most IPOX® Indexes surged into month-end during FED week, as strong earnings across bellwethers, lower US yields, a firmer Japanese Yen and muted commodities contributed to an acceleration of positive Equity Momentum, indicated by the sharp drop in equity risk (VIX: -7.38%). In the US., e.g., the IPOX® 100 US (ETF: FPX) - benchmark for the performance of US New Listings and respective M&A - soared +4.53% to -26.77% YTD, performing better than when compared to the S&P 500 (ETF: SPY) on a weekly and monthly basis. Big gains extended to most markets abroad, including the IPOX® 100 Europe (ETF: FPXE), IPOX® Nordic (IPND) and IPOX® MENA (IPEV) which all outperformed. Another dismal week for China-domiciled exposure amid political overhang and repatriation selling by foreign investors pressured the IPOX® International (ETF: FPXI), while IPO M&A continued to display a solid showing, with the IPOX® Growth Infusion (GNDX) trading in line with the benchmarks.

IPOX® Portfolio Holdings in Focus

Amid a big divergence in performance across individual sectors with Information Technology significantly outperforming Health Care, we note strong gains in some of the very recent portfolio additions, including 01/2022 IPO communications equipment maker Credo Technology (CRDO US: +42.41%), 01/2022 Spin-off utility Constellation Energy (CEG US: +22.41%) and 02/2022 IPO energy explorer 05/2022 IPO Profrac (PFHC US: +17.29%), which led the IPOX® 100 US (ETF: FPX) leaderboard. Here, disappointing earnings pressured infrastructure software maker 07/2018 IPO Tenable Holdings (TENB US: -20.78%) and health care services provider 05/2019 IPO Avantor (AVTR US: -6.30%), e.g. In markets abroad, we note the fresh post-IPO high in the slew of European-domiciled firms linked to renewable energy, such as 06/2021 IPO Stockholm-based OX2 (OX2 SS: +15.68%), Porto-based 07/2021 IPO Greenvolt Energias Renovaveis (GVOLT PL: +9.02%) and Madrid-based 07/2021 IPO Corporacion Acciona Energias Renovables (ANE SM: +8.31%), e.g.

Global IPO Deal Flow Review and Outlook

9 sizeable IPOs launched last week, with the average equally weighted deal gaining +11.20% based on the difference between the final offering price and Friday’s close. ECB Bancorp (ECBK US: +39.80%), holding company for Everett Co-operative Bank was the only US listing, raising $106m. Internationally, Thai Life (TLI TB: -5.00%) stood out for raising $1 billion in Bangkok, the largest IPO YTD in the country. On Tuesday, four Chinese firms listed in Switzerland, which has been attracting Chinese firms amid regulatory tightening the US. The three battery companies Ningbo Shanshan (SSNE SW: -0.19%), GEM (GES SW: +5.05%), and VW-backed Gotion High-Tech (GOTION SW: +0.00%), as well as building materials company Keda Industrial Group (KEDA SW: -0.21%), together raised more than $1.2b through the sale of depository shares. In South Korea, lithium battery recycling firm Sungeel Hitech (365340 KS: +84.00%) surged after previously becoming the country’s most oversubscribed IPO ever. Other IPOs included Spanish Investment Manager Axon Partners (APG SM: -2.09%) and South Korean electronic components maker ICH (368600 KS: -20.59%). Three IPOs are lined up for this week: Monday: South Korean power plant maintenance firm Soosan Industries (126720 KS, $154m raise) and Italian renewable energy firm Energy (ENY IM, $32m raise). Tuesday: IT management firm Japan Business Systems (5036 JP, $27m raise).

Other News include: 1) Ginkgo Bioworks (DNA US, 02/2011 IPO) to buy Zymergen (ZY US, 04/2021 IPO) for $300m. 2) Labcorp (LH US) to spin-off clinical development business. 3) Eutelsat (ETF FP) to merge with UK’s OneWeb in $3.4b deal to rival SpaceX’s Starlink. 4) JetBlue (JBLU US) acquires Spirit Airlines (SAVE US) for $3.8b. 5) 3M (MMM US) to spin-off $8.6b healthcare unit. 6) Cybersecurity unicorn Exterro targets 2023 IPO. 7) Saudi Arabia plans 2024 IPO for $500b NEOM project. 8) Porsche eyes 50% stake in Red Bull’s Formula One technology unit. 9) ThaiBev (THBEV SP) signals uncertainty over proceeding with $1b IPO of BeerCo unit. 10) Jack Ma gives up control of Ant Group in move seen as effort to appease regulators and expedite IPO plans. 11) Instacart reignites Q4/2022 IPO plans despite recent drops in valuation.

The IPOX® SPAC

The IPOX® SPAC (SPAC), currently composed of a selected 50 high conviction plays trading at both the pre- and post-consummation stage, added a massive +8.32% to -15.09% YTD last week. IPOX® SPAC Leaders recording notable upside/downside moves included newly merged picture content platform Getty Images (GETY US: +179.68%), while EV maker Lucid (LCID US: -7.32%) fell. Other SPAC news from last week: 1) 5 SPACs Announced Merger Agreement include a) Athena Consumer Acquisition (ACAQ US: +0.30%) with EV maker e.GO and b) DHC Acquisition (DHCA US: +0.20%) with fintech GloriFi. 2) 4 SPACs Approved Business Combination include a) CHW Acquisition (CHWA US: +1.20%) with dog walk service platform Wag (PET US: TBA) and b) Duddell Street (DASC US: -15.87%) with public policy and market regulatory information data platform FiscalNote (NOTE US: 08/01). 3) 1 SPAC Terminated Merger include a) Abri SPAC I (ASPA US: +0.20%) with blockchain company Apifiniy Group. 4) 2 SPACs opted to liquidate include a) SCVX Corp (SCVX US: +0.10%) at $10.03/shares and b) Gobi Acquisition (GOBI US: +0.30%) at $10.01/share. 5) No new SPAC launched last week in the U.S.