The IPOX® Week #723

IPOX® Indexes trump benchmarks on strong earnings, lower yields.

Heavyweight Constellation Energy soars, IPOX® MENA rises to fresh record.

New Product Launch:

IPOX® proudly launches the IPOX® Bond Indexes.

Read the latest

IPOX® Watch Pre-IPO Analysis on Reddit.

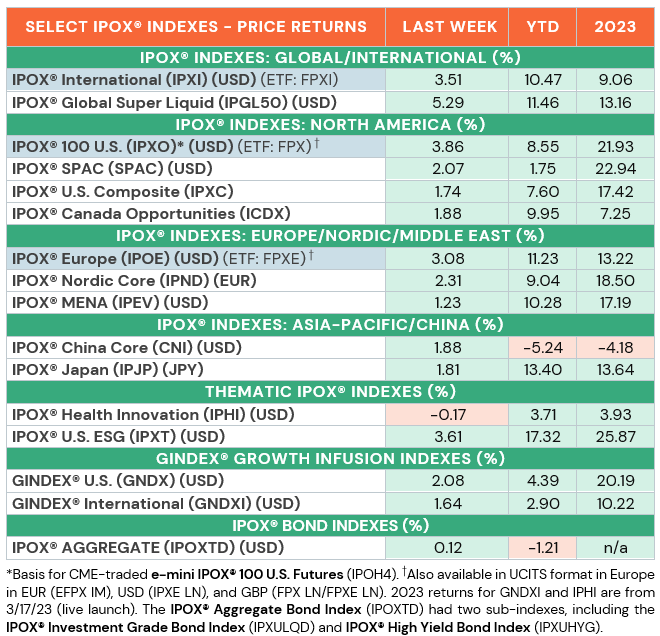

IPOX® PERFORMANCE REVIEW: Good earnings across most of our portfolio holdings, big crypto and AI-momentum and declining government bond yields - reflected in higher bond prices of debt issued by IPOX® Holdings and captured in the IPOX® Aggregate Bond Index (IPOXTD: +0.12%) - as well as lower risk (VIX: -4.65%) drove the IPOX® Indexes to big gains towards the beginning of the month. On the global level, e.g., the super-liquid IPOX® Global 50 (IPGL50) - composed of the largest and most liquid IPOs, Spin-offs and IPO M&A by applying the IPOX® Indexes Technology - soared +5.29% to +11.46% YTD, outpacing the MSCI World (MXWD) by a massive +466 bps. Big gains extended across global regions with the IPOX® 100 U.S. (IPXO) adding +3.86% to +8.55% YTD, now handily beating the S&P 500 (SPX) YTD, while the IPOX® 100 Europe (IPOE) also soared anew. Amid strong initial returns for IPOs in the Middle East, we also note the fresh All-Time High in the IPOX® MENA (IPEV), benchmark for the most liquid and largest New Listings in the region. New economy stocks drove the portfolio higher last week, adding +1.23% to +10.28% YTD, to a fresh record. Firms pursuing IPO M&A pooled in the super-liquid and well diversified IPOX® Growth Infusion Indexes (GNDX, GNDXI) also rose and outperformed their respective benchmarks last week with the U.S.-domicile-focused version (GNDX) adding +2.08% to +4.39% YTD, while the International version (GNDXI) rose by +1.64% to +2.90% YTD.

IPOX® PORTFOLIO HOLDINGS IN FOCUS: Amid upcoming March 15th Futures and Option expiration positioning activity and (post)-earnings Momentum, the divergence in the return distribution across IPOX® Holdings remained significant. In the IPOX® Global 50 (IPGL50) and IPOX® 100 U.S. (IPXO), e.g., the story of the week belonged to the big week in beleaguered language app 07/21 IPO Duolingo (DUOL US: +33.51%) and best-in-class ESG alternative energy play 01/22 Spin-off USD billion 54 Constellation Energy (CEG US: +26.87%) which now has surpassed parent company Exelon’s (EXC US: -0.72%) market cap which in turn may motivate more corporate actions around (alternative) energy firms. Good earnings and the decision of iPhone maker Apple (APPL US: -1.57%) not to enter the EV market also drove big strength in a number of auto makers, foremost Chinese electric car maker 07/20 IPO Li Auto (LI US: +25.11%), as well as Germany’s 12/21 IPO Daimler Truck Holdings (DTG GY: +21.68%) whose stock and U.S.-traded and IPOX®-held bonds rose strongly last week. IPOX®-tracked firms trading off the exuberant sentiment for crypto continued to soar, with crypto exchange operator 04/21 Direct Listing Coinbase (COIN US: +23.97%) and trading platform 07/21 IPO Robinhood (HOOD US: +14.50%) in focus. Finally, we note the exceptional week for serial IPO acquirer Samsonite International (1910 HK: +17.99%), a key component in the IPOX® International (IPXI), as well as in the IPOX®-managed Rakuten Global IPO Fund, an active fund available to investors in Japan, including NISA. Amid speculation of a potential H.K. delisting and takeover of the firm, the owner of the TUMI luggage brand soared last week to the highest level since 08/18. Disappointing results and management changes pressured 09/20 IPO cloud services provider Snowflake (SNOW US: -18.58%), application software maker 09/20 IPO Unity Software (U US: -7.52%) and recent German IPO sandals maker Birkenstock BIRK US: -8.02%).

LIVE LAUNCH OF THE IPOX® BOND INDEXES: The IPOX® Bond Indexes are now live, offering access to U.S. dollar-denominated corporate debt from the IPOX® Universe. Designed for both passive and active financial products, these indexes aim to capture the unique returns and potential outperformance of new listings. For more information, contact info@ipox.com.

IPO ACTIVITY AND OUTLOOK: 33 accessible New Listings priced last week, with the average (median) equally-weighted deal (non-direct listings and de-SPAC) adding +59.95% (+21.72%) based on the difference between the final offering price and the Friday’s close. The largest deals were seen by Indian Hyatt partner Juniper Hotels (JUNIPER IN: +27.72%, $217m offer) and Saudi Arabian pharma firm Avalon Pharma (AVALONPH AB: +119.27%, $131m offer), which surged amid continuing appetite for listings in the MENA region. One listing launched in the U.S., Nevada solar energy firm SolarMax Technology (SMXT US: +22.25%, $18m offer). The micro-IPO of Italian solar energy firm Espe (ESPE IM: +240.00%, $2.3m offer) was the only European listing last week, while three firms started trading in Japan, most notably Venture Capital-backed AI manufacturing solutions provider VRAIN Solution (135A JP: +102.01%, $22m offer), which doubled to $400m market cap. No significant IPOs are planned for next week, read the latest IPOX® Watch Pre-IPO Analysis on upcoming listing candidate, social media website Reddit (RDDT US).

IPOX® SPAC INDEX (SPAC): The Index added +2.07% last week to +1.75% YTD. Telehealth platform Hims & Hers (HIMS US) soared +37.76% after strong earnings and rapid growth, while insurer/reinsurer specialist International General Insurance (IGIC US) fell -8.76% despite solid earnings. 3 SPACs have entered into a definitive merger agreement include SK Growth Opportunities (SKGR US) announced a merger with online trading platform Webull at an implied enterprise value of $7.3 billion, largest since 2023. Crypto mining company BitFuFu (FUFU US) closed 2022 announced deal with Arisz Acquisition and began trading. No SPACs announced liquidation. No new U.S. SPAC launched last week.

Follow our IPO Calendar and social media channels (e.g. Linkedin) for Updates.