The IPOX® Week #733

IPOX® Equity Indexes extend YTD gains ahead of May expiration week.

IPOX® Corporate Bond Indexes stable. U.S. inflation report lined up.

No margin for error as select IPOs diverge widely after earnings.

Amid big IPO interest, UAE’s Spinney debuts only mildly positive.

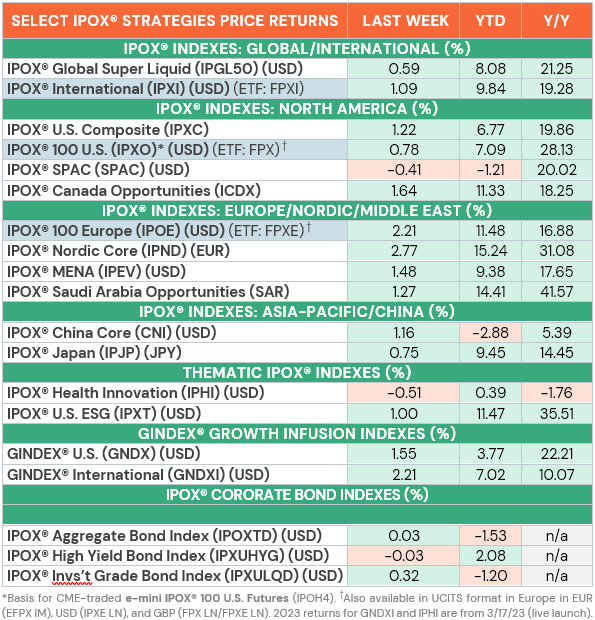

IPOX® REVIEW: Ahead of U.S. May options expiration week and more updates on inflation, most IPOX® Equity Indexes extended last week’s strong gains to trade higher. Amid some rates pressure into the weekend and mixed earnings amongst IPOX® High-Growth Stocks, however, select exposure lagged the derivatives-heavy benchmarks across Europe and the U.S. which were propelled by post-earnings Momentum-Buying amid plunging equity risk (VIX: -6.97%).

In the U.S., e.g., the IPOX® 100 U.S. (ETF: FPX), benchmark for the most innovative U.S. companies as measured by IPOs and Spin-offs, added +0.78% to +7.09% YTD, lagging the benchmarks between -107 bps. (SPX) and -40 bps. (RTY), however, well ahead of actively managed innovation gauges (ARKK: -5.61%). The IPOX® Corporate Bonds Indexes traded flat, with the IPOX® High Yield Corporate Bond Index (IPXUHGY) maintaining its big relative performance lead vs. conventional U.S. High Yield Corporates YTD, e.g.

Markets pooling non-U.S. domiciled exposure outpaced U.S. equities last week: Top of the list ranked the IPOX® Nordic (IPND) which added +2.77% to +15.24% YTD, finishing the week at a fresh multi-year high and also propelling the IPOX® 100 Europe (ETF: FPXE) and IPOX® International (ETF: FPXI). Gains extended to all other IPOX® Regional Indexes, including the IPOX® Canada (ICDX). After some consolidation and ahead of more ECM activity, we note renewed momentum in the IPOX® MENA (IPEV), innovative benchmark for the performance of the most liquid and best performing IPOs across the UAE and Saudi Arabia.

Acquirers of IPOs pooled in GINDEX® traded well, with strong earnings propelling GINDEX® International (GNDXI) by a large +2.21% to +7.02% YTD., e.g. ![]()

Amid earnings, returns of individual portfolios holdings pooled in the IPOX® 100 U.S. (ETF: FPX) remained widely dispersed with no margin for error for high-growth exposure in particular. Here, big earnings-driven declines in language app Duolingo (DUOL US: -21.62%), gaming platform Roblox (RBLX US: -19.85%) and AI-play Palantir Technologies (PLTR US: -11.70%) failed to derail otherwise positive Momentum as AI salad bar operator Sweetgreen (SG US: +42.81%), IBM Spin-off IT Services Provider Kyndryl (KD US: +32.77%), Everything AI-play S&P 500 (SPX) inclusion candidate Applovin (APP US: +15.13%), payment app great comeback-story Toast (TOST US: +17.99%) and social media play Reddit (RDDT US: +14.77%) delivered big upside surprises, while select climate/energy stocks rallied anew, such as Constellation Energy (CEG US: +10.30%) and NRG (NRG US: +9.13%).

Across the list of non-U.S. domiciled stocks, we note another volatile week for some of the most recent IPOs, some of them traded in the U.S. Top of the list ranked Norway’s oilfield services provider small-cap DOF Group (DOF NO: +15.38%), while speculation about a corporate action propelled IPOX® International (ETF: FPXI) heavyweight UK-based, U.S.-traded Industrial Nvent (NVNT US: +7.71%) to a fresh weekly post-IPO high and semiconductor technology provider ARM Holdings (ARM US: +7.02%) managed to recover more of the recent losses suffered during April U.S. options expiration week. Italian glass container maker, U.S.-traded Stevanato (STVN US: -17.50%) and Tokyo-traded innovative Financial Services Provider M&A Research (9552 JP: -2.50%) recorded notable declines, while drilling services provider ADES (ADES AB: -7.91%) and Saudi Stock Exchange Operator Saudi Tadawul Group (TADAWUL AB: -5.44%) pressured the otherwise strongly outperforming IPOX® MENA (IPEV).

IPOX® SPAC Index (SPAC): The index fell -0.41% last week to -1.21% YTD amid earning season volatility. Outliers included mobile banking app MoneyLion (ML US: +14.59%), while Blackstone-backed human capital solution provider Alight (ALIT US: -17.53%) plunged. WinVest Acquisition (WINV US) extended its termination date as it announced to merge with geolocation-based buy-and-sell marketplace Xtribe, while Sam Altman-backed SPAC Alt Acquisition completed its merger with mini nuclear fusion reactor company Oklo (OKLO US: -43.02%). SPAC Issuing activity picked up with one deal getting done last week.

ECM REVIEW AND OUTLOOK: 5 significant IPOs debuted across the global regional last week with the average (median) equally-weighted deal adding +31.31% (+5.88%) based on the difference between the final offering price and Friday’s close. Amid exuberant initial investor demand, the IPO of UAE retailer Spinney’s (SPINNEYS UH: +5.88%) debuted only mildly positive, underlying the recent trend of lackluster immediate IPO returns across MENA. U.S.-based firms (SVCO US, PAL US) were priced to perfection, while the good initial showing of China-EV maker ZEEKR (ZK US: +34.57%) provides much relief for the hard-hit China-U.S. IPO ties. More foreign-domiciled firms are lined up to debut in the U.S. this week with the largest deal belonging to UK-based video games maker Games Global (GGL US). Follow our IPO Calendar and social media (e.g. LinkedIn) for the complete list and respective Updates.